The rapid evolution of BioPharma Corporate Venture Capital Investment

Dive deeper

Ever feel like BioPharma Corporate Venture Capital (CVC) investment trends change too quickly? One year it’s AI, the next it’s cell and gene therapy. The latest cross-portfolio scan of Google and 22 biopharma Corporate Venture Capitals shows a clearer pattern: data-first platforms and next-gen therapeutics are no longer “experimental”—they’re the main event.

GV most active (60+); AbbVie leads exits; AI/Digital, small molecules, CGT, antibodies dominate; Oncology ~23% — Global, 2023–2025, announced rounds, USD.

Here’s a quick video summary of our 2025 analysis, highlighting the key trends and shifts in Biopharma Corporate Venture Capital (CVC) investment. Want the full insights? 📥 Download the full report: https://bit.ly/46zutfv

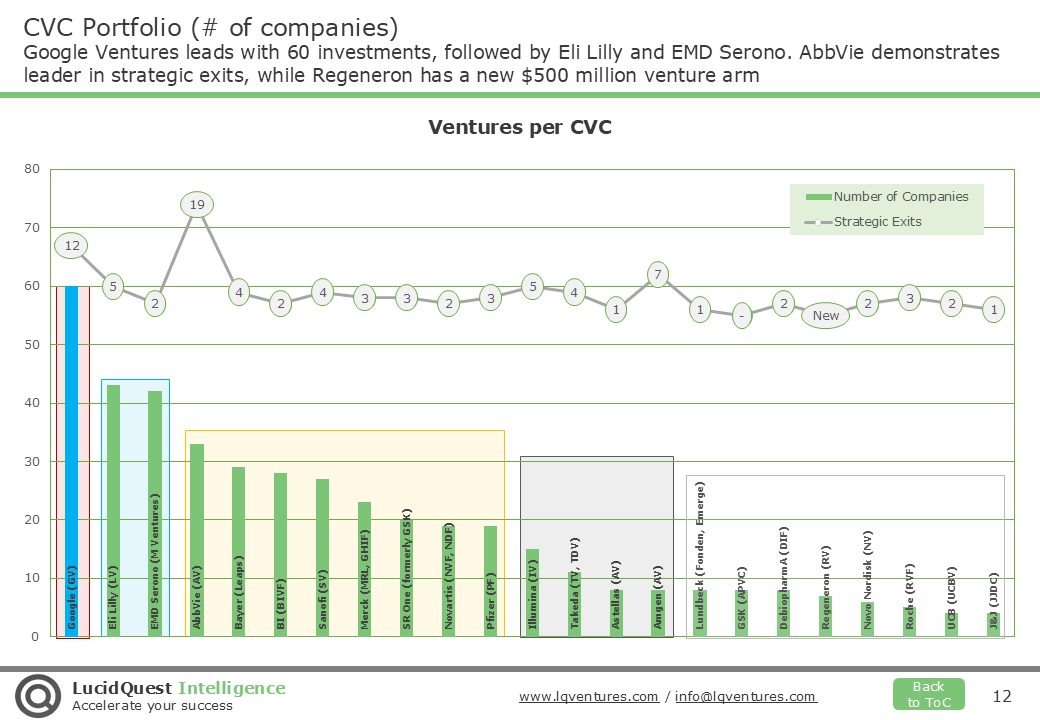

Who’s Leading Biopharma CVC Investments in 2023–2025?

- Google Ventures (GV) holds a clear lead with 60+ investments, retaining the #1 spot across both 2020–2023 and 2023–2025.

- Eli Lilly (Lilly Ventures) shows steady momentum with 19 investments.

- EMD Serono (M Ventures) continues its climb with 12 investments.

- AbbVie stands out for the highest number of strategic exits (portfolio size 7), underscoring outcome quality over sheer volume.

Takeaway: Volume crowns GV the activity leader; exits spotlight AbbVie’s strategic sharpness.

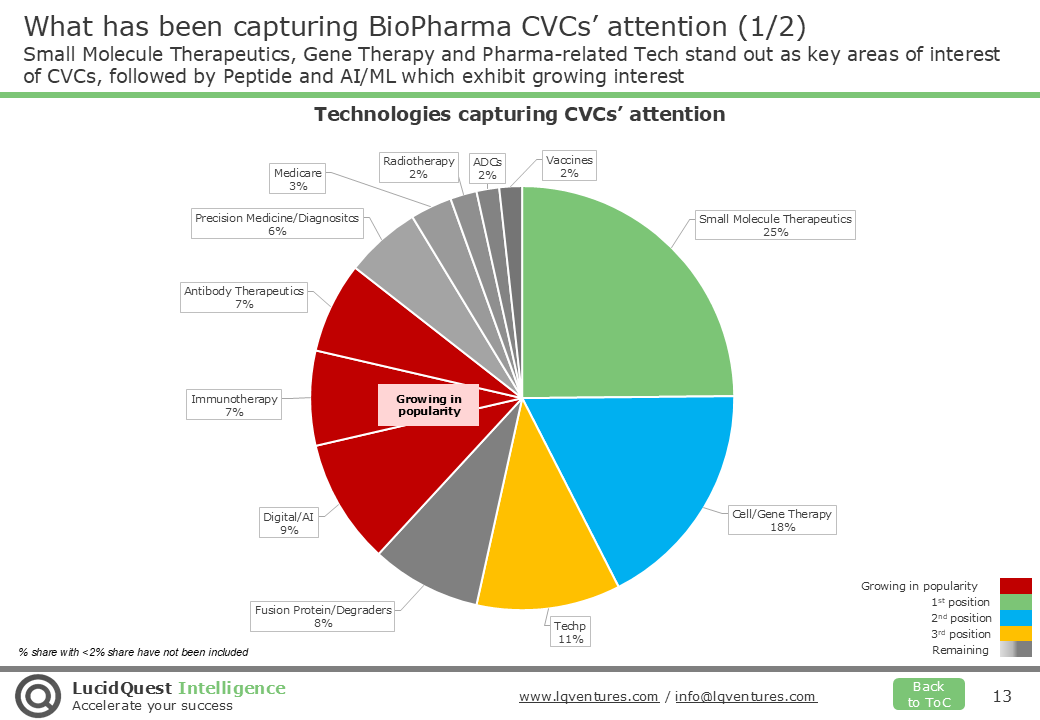

What biopharma CVCs are betting on (2023–2025). Technonoly Priorities and Top Therapeutic Areas

Tech priorities

- Digital & AI/ML: Remains the top priority for biopharma CVCs, moving from pilot projects in 2023 to mainstream adoption in diagnostics and clinical decision support by 2025.

- Small-Molecule Therapeutics: Continues to be a resilient focus, with AI increasingly accelerating drug discovery and development.

- Gene & Cell Therapy: Maintains strong interest, shifting toward novel delivery methods, including in vivo approaches and RNA-targeted therapies.

- Antibody-Based Approaches: Rising priority, emphasizing multi-specific antibodies and next-generation formats.

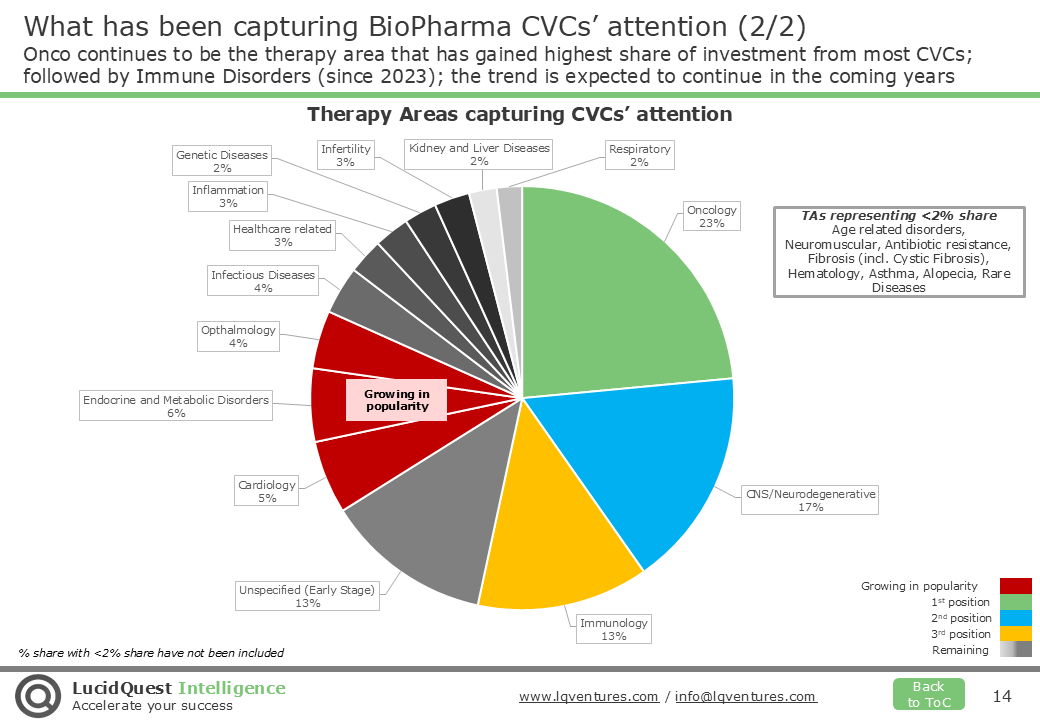

Therapeutic areas (TAs)

- Oncology dominates.

- Immune disorders expand rapidly.

- CNS/Neurodegeneration remains a sustained bet.

- Women’s health, rare genetic diseases, and advanced digital therapeutics show accelerating interest.

Pattern you can feel: Data + delivery + precision—the triad defining the new tranche of winners.

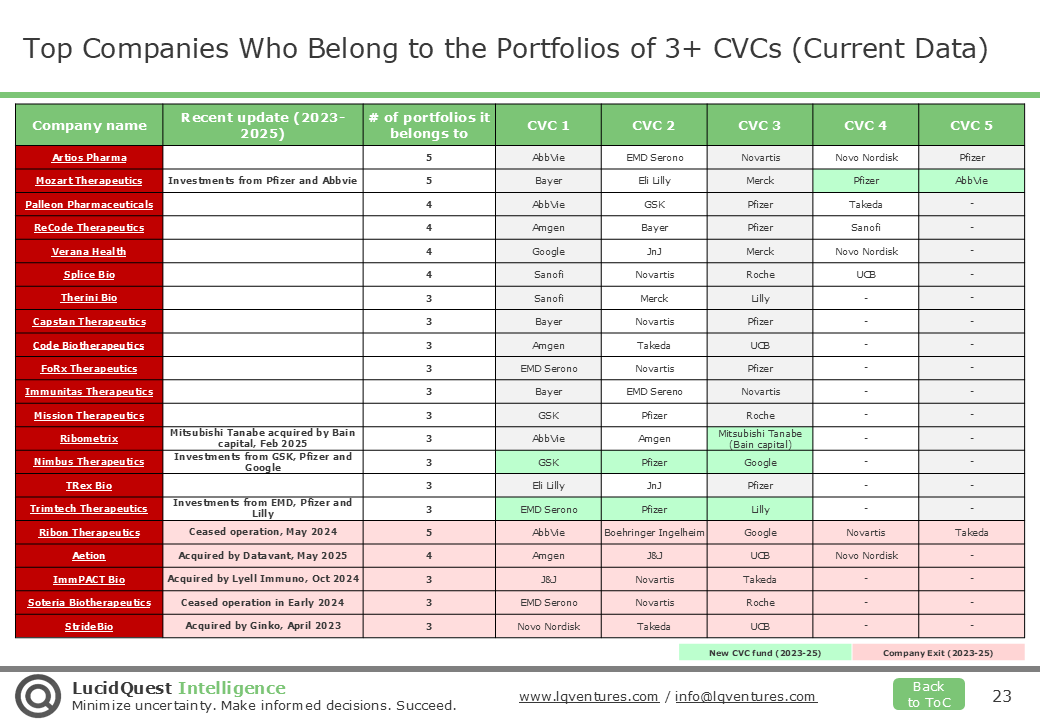

Signals from shared portfolios (social proof you can quantify)

When a company appears in ≥3 CVC portfolios, it sends a powerful “market-validity” signal.

- 5 portfolios:

Artios Pharma (AbbVie, EMD Serono, Novartis, Novo Nordisk, Pfizer)

Mozart Therapeutics (Bayer, Eli Lilly, Merck, Pfizer, AbbVie)

Ribon Therapeutics (AbbVie, Boehringer Ingelheim, Google, Novartis, Takeda)

- 4 portfolios:

Palleon Pharmaceuticals, ReCode Therapeutics, Verana Health, Splice Bio, Aetion

- 3 portfolios:

Therini Bio, Capstan Therapeutics, Code Biotherapeutics, FoRx Therapeutics, Immunitas Therapeutics, Mission Therapeutics, Ribometrix, Nimbus Therapeutics, TRex Bio, Trimtech Therapeutics, ImmPACT Bio, Soteria Biotherapeutics

Why it matters: Repeated selection across CVCs = cross-strategic relevance + de-risked diligence for new investors and strategic partners.

Who explores the broadest tech + TA frontiers?

Most technologies explored (VI-TF): 1) Eli Lilly, 2) Boehringer Ingelheim, 3) Google

Most diverse TAs (VI-TAF): 1) Google, 2) Eli Lilly, 3) Sanofi

Overall “Explorer” Index (VI-TF + VI-TAF, 2025): 1) Google, 2) Eli Lilly, 3) Sanofi

Decoding the indices:

VI-TF = how many distinct technology modalities your portfolio touches.

VI-TAF = how many therapeutic domains you cover.

Explorer = balanced breadth across both—a proxy for optionality and future-proofing.

Corporate Venture Capital in Pharma: Tracking Funding Across Therapies and Technologies

AbbVie (AbbVie Ventures)

Backs small-molecule and antibody therapeutics while selectively exploring gene & cell therapy; Oncology and CNS remain the core priorities.

Amgen (Amgen Ventures)

Focus on CGT, protein/degraders, and enabling tech, with rising interest in Digital/AI and small molecules; Oncology leads, with selective CNS bets.

Astellas (Astellas Ventures)

Invests in CGT, small molecules, Digital/AI, and antibodies; primary focus on Oncology and Neuroscience, with interest in Ophthalmology and Cardiology.

Bayer (Leaps by Bayer)

Growing exposure to CGT, small molecules, and Digital/AI; anchors in Oncology, Autoimmune, and Respiratory/Inflammatory disorders, while scanning adjacent areas.

Boehringer Ingelheim (BI Venture Fund)

Emphasizes Immunotherapy, then antibiotics, CGT, and small molecules; targets Oncology, Antimicrobial Resistance, and Autoimmune disorders.

Debiopharm (DIF)

Early- to growth-stage investor in digital health, AI, and tech platforms; concentrates on Oncology, immune disorders, and metabolic diseases.

Eli Lilly (Lilly Ventures)

Centers on small molecules and CGT across Neurodegeneration, Oncology, Cardiovascular, and Autoimmune indications.

EMD Serono (M Ventures)

Prioritizes small molecules and Digital/AI with added CGT interest; main areas are Oncology and Neurodegenerative disorders.

Google (GV)

Heavy tilt toward Digital/AI and platform tech, with selective small-molecule and CGT plays; portfolio spans many TAs, notably Oncology and Infertility.

GSK (APVC)

Backs medical devices and enabling platforms; favors early-stage CNS, immune-related, and oncology therapies, especially where digital or novel delivery is integral.

Illumina (Illumina Ventures)

Targets antibody therapeutics, CGT, precision diagnostics, and small molecules; early portfolio breadth with focus on Oncology, Fibrosis, and antibiotic resistance.

J&J (JJDC)

Diversified across vaccines and drug delivery; Oncology is largest focus, with emphasis on prostate cancer and allergy.

Lundbeck (Lundbeckfonden, Emerge)

Balanced across CGT, immunotherapy, proteins, and small molecules; TAs include Oncology, Hematology, Immunology, Infertility, and Microbial diseases.

Merck (MRL Ventures, Impact Venture Fund, MSD GHI Fund)

Invests in immunotherapy, antibodies, fusion proteins/degraders, and tech; Oncology leads, alongside CNS, Autoimmune, Neuromuscular/Somatic, and Ophthalmology.

Novartis (Novartis Venture Fund, Novartis Digital Fund)

Strong in small molecules and antibodies; focuses on Oncology, Autoimmune, and Ophthalmology, plus digital health, biomarkers, and patient-engagement tech.

Novo Nordisk (Novo Ventures)

Primary focus on small molecules and protein therapeutics; invests across Endocrine & Metabolic and Cardiology, with equal interest in liver disease, obesity, neurodegeneration, diabetes, and rare endocrine disorders.

Pfizer (Pfizer Ventures)

Dual emphasis on small molecules and CGT, plus antibodies/bispecifics; Autoimmune and Oncology together comprise over half of priorities.

Regeneron (Regeneron Ventures)

Launched April 2024; focuses on gene therapy, RNA, and small molecules across Oncology, CNS, Ophthalmology, and enabling platforms—mirroring Regeneron’s delivery strengths.

Roche (Roche Venture Fund)

Concentrates on protein and small-molecule therapeutics; key areas include Autoimmune, CNS/Neuroscience, Neuromuscular, and Cardiovascular diseases.

Sanofi (Sanofi Ventures)

Invests in small molecules, CGT, and antibodies with rising Digital/AI interest; primary focus on Oncology, Autoimmune, and Neurodegenerative disorders.

SR One (formerly GSK SR One)

Leans into small molecules and CGT with immunotherapy interest; priorities span Oncology, CNS, and Autoimmune, plus broader metabolic/respiratory exploration.

Takeda (Takeda Ventures & Takeda Digital Ventures)

Focuses on CGT and small molecules in Oncology, CNS, and Rare diseases, complemented by digital health to improve outcomes.

UCB (UCB Ventures)

Low-activity fund emphasizing CGT, protein, and nanoparticle tech; therapeutic focus on Neurology/CNS and genetic disorders.

📊 Acess the full Report 📥 https://bit.ly/46zutfv

📢 Stay Ahead in BioPharma CVC trends!

✅ Contact LucidQuest at info@lqventures.com for strategic insights on BioPharma venture strategy.

FAQs

Which biopharma CVC is most active in 2023–2025?

GV (Google Ventures) leads by volume with 60+ investments across 2023–2025, retaining the top spot from 2020–2023 into 2023–2025. [

Which pharma CVC shows the strongest exit track record?

AbbVie Ventures is highlighted for the highest number of strategic exits, prioritizing outcome quality over portfolio size (portfolio size 7).

Are AI and digital health still top priorities for biopharma CVCs in 2025?

Yes. AI/Digital has progressed from pilots in 2023 to mainstream use in diagnostics and clinical decision support by 2025.

What drug modalities are biopharma CVCs funding most right now?

AI/Digital, small molecules, gene and cell therapy, and antibody-based approaches are the dominant focus areas.

Which therapeutic area attracts the most biopharma CVC funding?

Oncology leads at about 23% of activity. Immune disorders and CNS are expanding, with growing interest in women’s health, rare genetic diseases, and advanced digital therapeutics.

Which startups are backed by multiple pharma CVCs?

Five-portfolio names include Artios Pharma, Mozart Therapeutics, and Ribon Therapeutics. Four-portfolio examples include Palleon, ReCode Therapeutics, Verana Health, and Splice Bio.

Which corporate VCs explore the broadest tech and disease spaces?

Explorer index: Google ranks first overall, followed by Eli Lilly and Sanofi. Google and Lilly lead individual breadth measures.

Are small molecules still a priority for pharma venture investors?

Yes. Small-molecule therapeutics remain resilient, with AI increasingly accelerating discovery and development.

What is the focus shift in gene and cell therapy for CVCs?

Interest persists, with a shift toward novel delivery, including in vivo approaches and RNA-targeted therapies.

Are multi-specific antibodies on the rise with pharma CVCs?

Yes. Antibody-based approaches are a rising priority, emphasizing multi-specific formats and next-generation designs.

Which CVCs lead in portfolio breadth across tech or TAs?

Most technologies explored: Eli Lilly, Boehringer Ingelheim, Google. Most diverse TAs: Google, Eli Lilly, Sanofi.